Capital Insights: What the Software Sell-Off Tells Us

Mar 18 2026 | Back to Blog List

VIDEO TRANSCRIPT:

Hi, I’m Trent Von Ahsen, partner with Cedar Point Capital Partners. Welcome to the March 2026 edition of Capital Insights.

This month, we’re looking at the recent sell-off in software stocks and what this tells us about how quickly market narratives can shift.

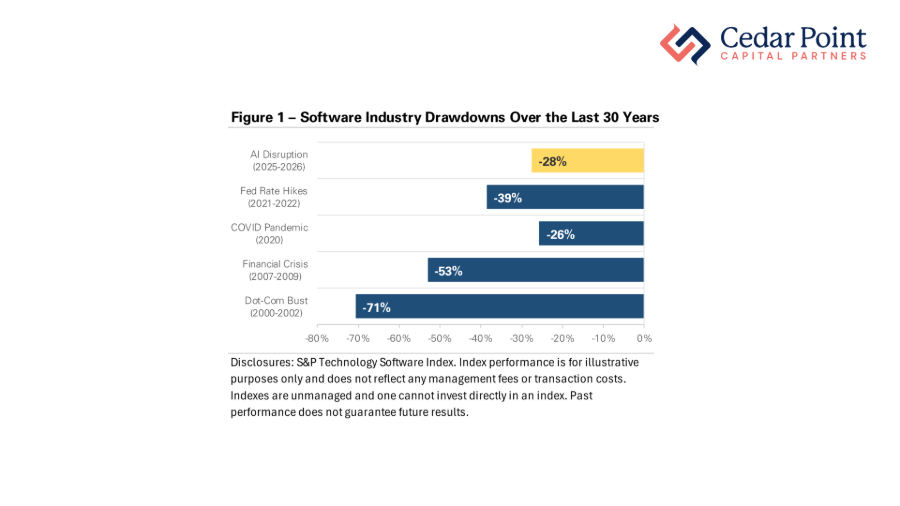

The software sector has declined nearly 30% from its peak last October. That makes it one of the largest non-recessionary drawdowns in more than three decades, as we can see in Figure 1.

Historically, the largest declines in software stocks occurred during recessions, like the dot-com bubble bust in the early 2000s or the great financial crisis in 2008, when corporate earnings were falling and businesses were cutting spending.

This time, however, is different.

The recent sell-off in software has largely been driven by artificial intelligence.

Over the past year, new AI products showed that general-purpose AI tools could perform tasks that previously required specialized software—and do it at a lower cost.

Markets reacted quickly to this.

Software stocks sold off first, but concerns soon spread to other industries, including financial data providers and logistics companies.

Investors previously saw AI as a productivity tool that could help companies operate more efficiently. But these new developments shifted the conversation toward a more disruptive possibility: that AI could replace entire categories of professional services.

By late February, that narrative began to cool and markets started to stabilize as analysts pushed back on some the most extreme scenarios.

But the broader question remains: which industries will be disrupted, and which will adapt?

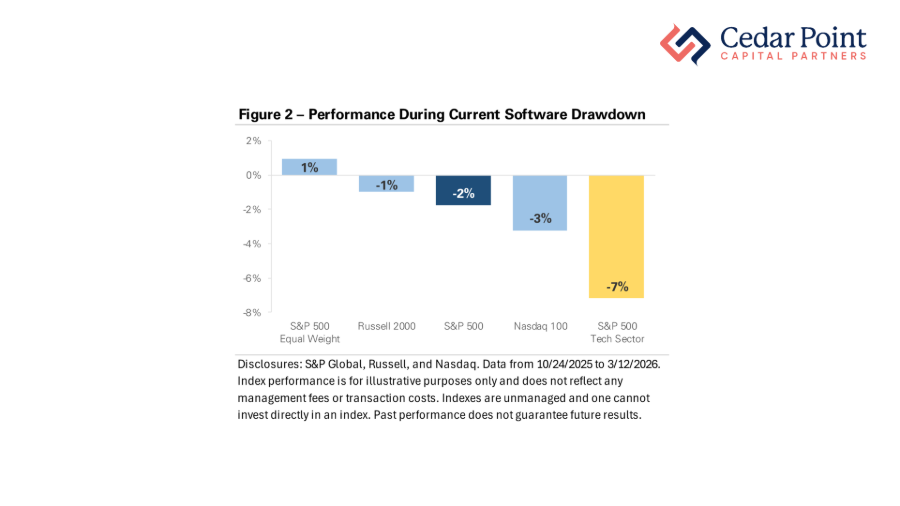

As we shift to Figure 2, what may possibly be the biggest lesson for investors over the past few months is that the impact has been far more limited for those with diversified portfolios.

While software stocks have declined sharply, international stocks and the average S&P 500 Index company have actually produced gains. Meanwhile, the broader S&P 500 Index, Small Caps, and the Nasdaq 100 Index are down only modestly.

The takeaway is a familiar one.

Even well-established industries can reprice quickly when expectations about future earnings change. But diversification across sectors and asset classes remains one of the most effective ways to navigate uncertainty and market volatility.

If you have any questions about this video or your portfolio, reach out and let’s start a conversation.

My name is Trent Von Ahsen, and I look forward to seeing you right here next month for our latest edition of Capital Insights.

Stay curious, stay mindful of your goals, and we’ll see you next time.

The commentary on this blog reflects the personal opinions, viewpoints, and analyses of Cedar Point Capital Partners (CPCP) employees providing such comments and should not be regarded as a description of advisory services provided by CPCP or performance returns of any CPCP client. The views reflected in the commentary are subject to change at any time without notice. Nothing on this blog constitutes investment advice, performance data or any recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Cedar Point Capital Partners manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results.