Tax Notes for 2022 (and Beyond) You Should Know

Mar 24 2023 | Back to Blog List

Taxes are fun for very few people, and we’re not necessarily in that category either, although Trent claims to like them. But we here at Cedar Point Capital Partners also recognize they’re an essential part of financial planning and wealth management, so we make sure to keep up with tax law changes that could impact your financial plan.

The most pressing thing you should know: the deadline to file your Federal Tax Return without an extension is Tuesday, April 18, 2023, courtesy of the weekend and a federal holiday on Monday. (It's coincidentally also Trent’s birthday, which may offer a possible explanation for his tax enjoyment.)

The most pressing thing you should know: the deadline to file your Federal Tax Return without an extension is Tuesday, April 18, 2023, courtesy of the weekend and a federal holiday on Monday. (It's coincidentally also Trent’s birthday, which may offer a possible explanation for his tax enjoyment.)

So you have a little breathing room if you’re taking it down to the wire this year.

April 18 is also the last day to make a contribution to various retirement accounts and health savings accounts, including individual retirement accounts (IRAs)—up to $6,000 this year, or $7,000 if you’re 50 or older—which could help you save money on your taxes thanks to their tax deductibility.

Otherwise, it feels like a transitional, in-between year for your taxes, especially if you live in our home state of Iowa. The federal tax credits and stimulus programs of the pandemic are winding down, taking some credits with them, while Iowa is about to begin its walk down to a 3.9% flat tax in 2026. This year also marks the end of taxation on retirement income for those 55 or older—a huge change for Iowa retirees.

Indeed, the changes to this year’s taxes may be small, but the cadence of change will be increasing in the years ahead. Here are a few notable changes we’re tracking and how you might want to respond.

Federal tax changes of note for TY2022

One of the biggest changes for the 2022 tax year is the sunsetting of certain pandemic-era tax breaks that Congress declined to extend. That includes the Child Tax Credit (CTC), which increased to as much as $3,600 in 2021 if you had a child five or younger; for 2022, it’s now falling back to its pre-pandemic limit of $2,000. The IRS has also reduced amounts for child- and dependent-care tax breaks which are used primarily by moderate- and low-income families.

Another change for 2022 involves the deductibility of charitable donations. If you use the standard deduction for 2022—a common decision for many filers now that it’s tied to inflation—you can no longer deduct charitable donations from your federal taxes.

That’s different from 2021 and 2020, when the IRS allowed taxpayers to deduct certain cash donations, even if they used the standard deduction. For those that do itemize, Congress declined to renew its temporary suspension of charitable-deduction limits, meaning that cash donations are now limited to 60% of your adjusted gross income (AGI), down from 100%.

This may impact your charitable giving plans in the coming years, but the AGI limits in place realistically limit how much this benefit is worth to our clients who itemize. There has been talk in Congress about bringing back the charitable giving benefit for taxpayers who don’t itemize, but it’s “something of a long shot,” according to Forbes.

For most, charitable giving will continue to be something you do to better the community, not for the tax benefits. But you may want to save those 2023 charitable giving receipts just in case.

Iowa tax changes of note for TY2022

If you really like to procrastinate finishing those state income tax returns, State of Iowa filers actually have until May 1, 2023 to file their 2022 return. This date is also the cut-off to make any last minute 529 Plan contributions for tax year 2022, another potential tax deduction opportunity for Iowa taxpayers.

Looking forward, Iowa is just starting out on a tax reform journey that promises to make our state more competitive, including a new flat tax and lower rates for corporations that will be phased in over the coming years.

A few of the biggest changes have already kicked in, however: As of January, Iowa is no longer collecting taxes on retirement income from qualified plans for those over 55, or farm rental income for retired farmers. That’s creating an exciting new era of affordability in the face of recent inflation for retirees here in the state (among the many other great reasons to live here).

According to the Iowa Department of Revenue, this new exemption includes income from:

- Governmental or other pension plans

- Defined benefit or defined contribution plans

- Annuities

- Individual retirement accounts (IRAs)

- Plans maintained or contributed to by an employer

- Deferred compensation plans or their earnings

For those still working, your state income taxes will be headed down over the next few years, although you won’t see much change in your returns for tax year 2022.

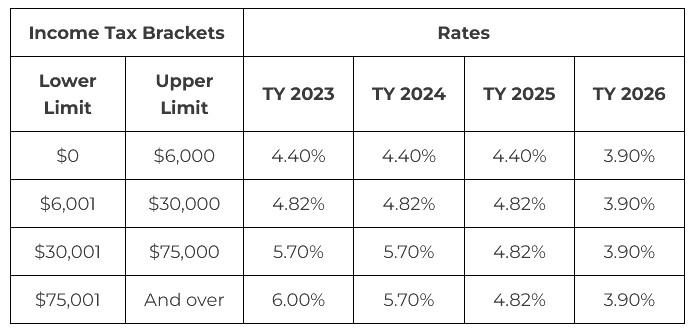

Starting with tax year 2023, those in the highest tax bracket ($75,001 and over) will see their rate fall from the current 8.53% down to 6%. As the years progress, rate relief will be phased in for lower brackets, until a flat rate of 3.9% is reached for tax year 2026. (See the below chart from the Iowa Department of Revenue.)

According to one estimate from the Tax Foundation, the median household income in Iowa (at $60,523) will see its income tax burden fall by roughly a quarter, from $2,765 to $2,052, by the time the flat tax is fully filled in. That’s more than $700 to the average family’s bottom line.

The new tax law also excludes capital gains from the sale or exchange of employer-owned stock from taxation (with certain provisions), giving a further boost for companies considering making the move toward employee ownership. That change will begin with the 2023 tax year, with 33% of capital gains exempted from taxation; by 2025, that exemption will reach 100%, making ESOP arrangements even more attractive for local companies.

Are your eyes glazing over yet? It’s OK, we get it. Let us help you handle the tax strategy so you can get back to the things that really matter in your life. Give us a call or reach out, and let’s grow your financial picture together.

The commentary on this blog reflects the personal opinions, viewpoints, and analyses of Cedar Point Capital Partners (CPCP) employees providing such comments and should not be regarded as a description of advisory services provided by CPCP or performance returns of any CPCP client. The views reflected in the commentary are subject to change at any time without notice. Nothing on this blog constitutes investment advice, performance data or any recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Cedar Point Capital Partners manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results.