Your Questions About OBBBA Tax Reform, Answered

Aug 15 2025 | Back to Blog List

When we look at the trends in our own web traffic, one thing becomes clear: tax planning is one of the most-read topics we cover here at Cedar Point Capital Partners. And it makes sense—few areas of wealth management are as complex or as consequential as taxes. You can choose not to follow the latest market trend or hot investment lead, but ignoring a tax law change can have lasting consequences for your future.

That's the case with the One Big Beautiful Bill Act (OBBBA), which reshapes tax rules for income, investments, deductions, and estate planning in the most sweeping reform since 2017.

That's the case with the One Big Beautiful Bill Act (OBBBA), which reshapes tax rules for income, investments, deductions, and estate planning in the most sweeping reform since 2017.

The law is sprawling, touching areas from educational expenses to qualified business income (QBI), and you need to have at least a passing understanding of how it could affect your financial plan in the years to come.

This month, we’ll focus on answering some of the most common questions about tax changes in the law, including key provisions affecting personal income, investment returns, and common deductions. Don’t see your question here? Reach out about your individual circumstances, and we can help evaluate how these change may apply to your situation.

Your OBBBA questions

- How does OBBBA affect tax rates?

- What tax deductions are changing under the OBBBA?

- Do I need to worry about the Alternative Minimum Tax (AMT) again?

- Has the estate and gift tax exemption changed?

- Have there been changes to buying or selling property?

- How does charitable giving change?

- What are the new "Trump Accounts" for kids I've heard about?

- Planning Strategies with OBBBA

First, a Few Definitions

Before we get started, let’s define a few key concepts and terms you’ll be seeing throughout this analysis piece:

One Big Beautiful Bill Act (OBBBA): The new federal law that makes wide-ranging changes to tax rates, deductions, estate planning, and savings rules.

Tax Cuts and Jobs Act (TCJA): The tax law passed in 2017 that lowered tax rates, increased the standard deduction, and introduced a cap on SALT deductions. Many provisions were set to expire at the end of 2025, which the OBBBA has extended or modified.

Adjusted Gross Income (AGI): Your total income from wages, investments, retirement accounts, and other sources, minus certain “above-the-line” deductions.

Modified Adjusted Gross Income (MAGI): AGI with certain income items added back in. For most taxpayers, it is the same or very close to AGI. MAGI determines your eligibility for many tax credits and deductions.

Above-the-Line Deductions: Deductions that reduce your AGI, such as HSA or pre-tax 401(k) contributions. These deductions are beneficial since they help you qualify for certain credits and other deductions.

Below-the-Line Deductions: Deductions that reduce your taxable income after AGI is calculated. While these deductions will not reduce your AGI (and therefore won’t help you qualify for other AGI-based thresholds), they ultimately reduce the amount of tax you owe.

Q. How does OBBBA affect tax rates?

One of the most notable ways that OBBBA affects tax rates is by keeping them right where they are. The law permanently extends the TCJA brackets—10%, 12%, 22%, 24%, 32%, 35%, and 37%—avoiding the scheduled jump to higher pre-2018 rates, including the old top bracket of 39.6%. That’s a welcome development for many American taxpayers who could have been facing a significant tax hike at the end of this year.

The law widens the 10% and 12% tax brackets slightly beginning in 2026 due to the inflation indexing base year being set back one year, delivering a modest break for some lower- and middle-income earners.

Q. What tax deductions are changing under the OBBBA?

The law makes changes to most existing Schedule A adjustments (itemized deductions), with the exception of the deduction for qualified medical expenses. It also adds five new below-the-line deductions, including for workers who earn income through tips and overtime, and a deduction for qualified auto loan interest. Here are the most notable changes:

Standard Deduction Increases

Starting in tax year 2025, the standard deduction rises to $31,500 for joint filers and $15,750 for single filers, with annual inflation adjustments thereafter. Compared to the standard deduction set for 2025 prior to the OBBBA, this is an increase of $1,500 for joint filers and $750 for single filers.

This continued expansion of the standard deduction is designed to simplify, encouraging more households to skip itemizing and simply take the flat deduction. For some taxpayers, that means fewer opportunities to benefit from itemized deductions—although the OBBBA’s new below-the-line deductions may be available regardless if you itemize or not.

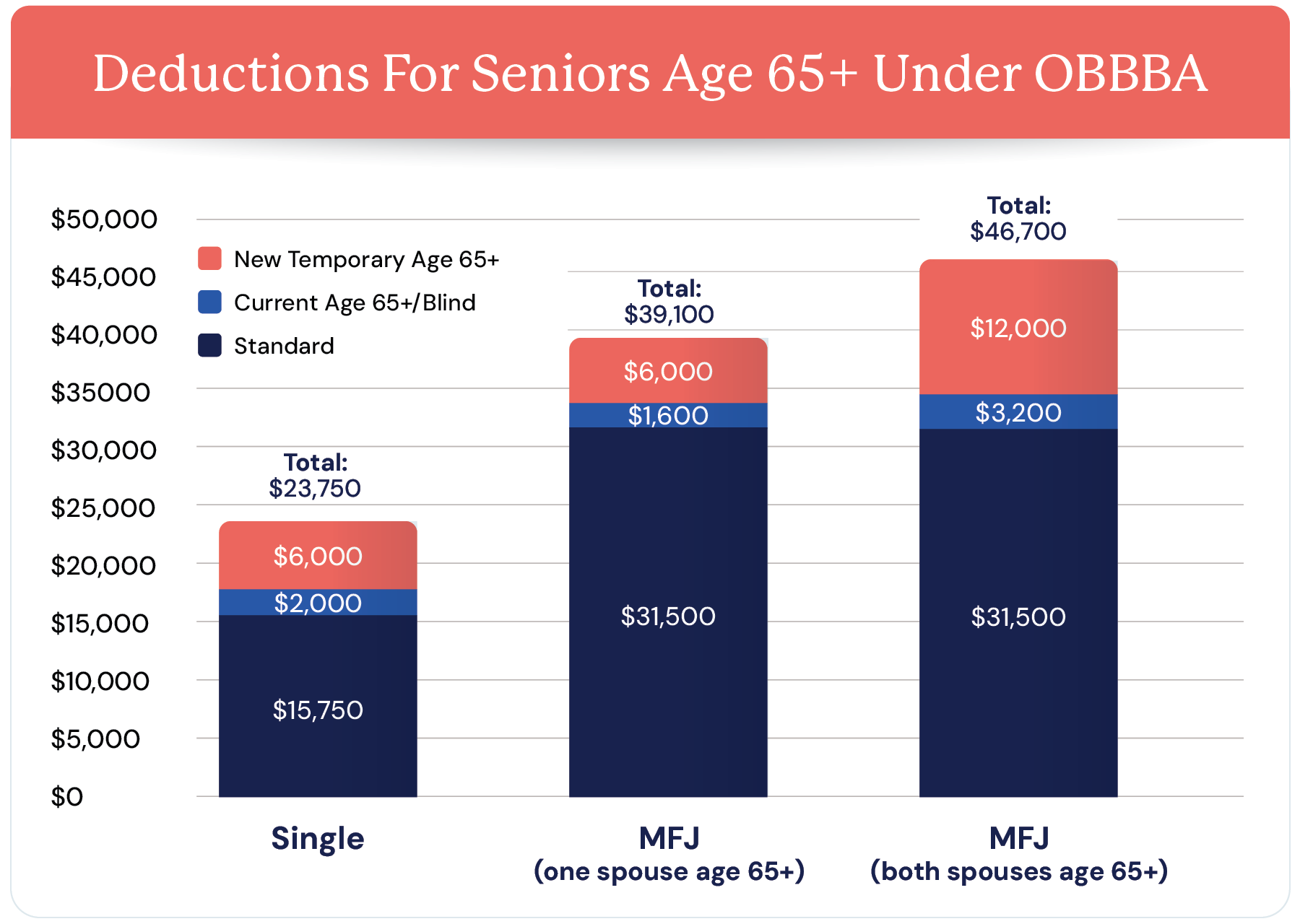

New Temporary Deductions for Taxpayers Age 65 or Older

The OBBBA adds a new $6,000 deduction for each taxpayer age 65 or older ($12,000 for qualifying couples) for tax years 2025–2028. This benefit applies whether you itemize or take the standard deduction, and stacks on top of the existing senior standard deduction, which adds another $1,600 per spouse if you are each age 65 or older.

The deduction phases out starting at $75,000 MAGI for single filers and $150,000 for joint filers, and phases out entirely at $175,000 and $250,000 respectively, making it a temporary but valuable tax break for seniors age 65 or older with moderate incomes.

For example, a 67-year-old married couple in 2025 could stack three deductions—the standard deduction ($31,500), the ongoing senior deduction ($3,200 total), and the new OBBBA senior deduction (up to $12,000)—for potentially over $46,000 of deductions alone.

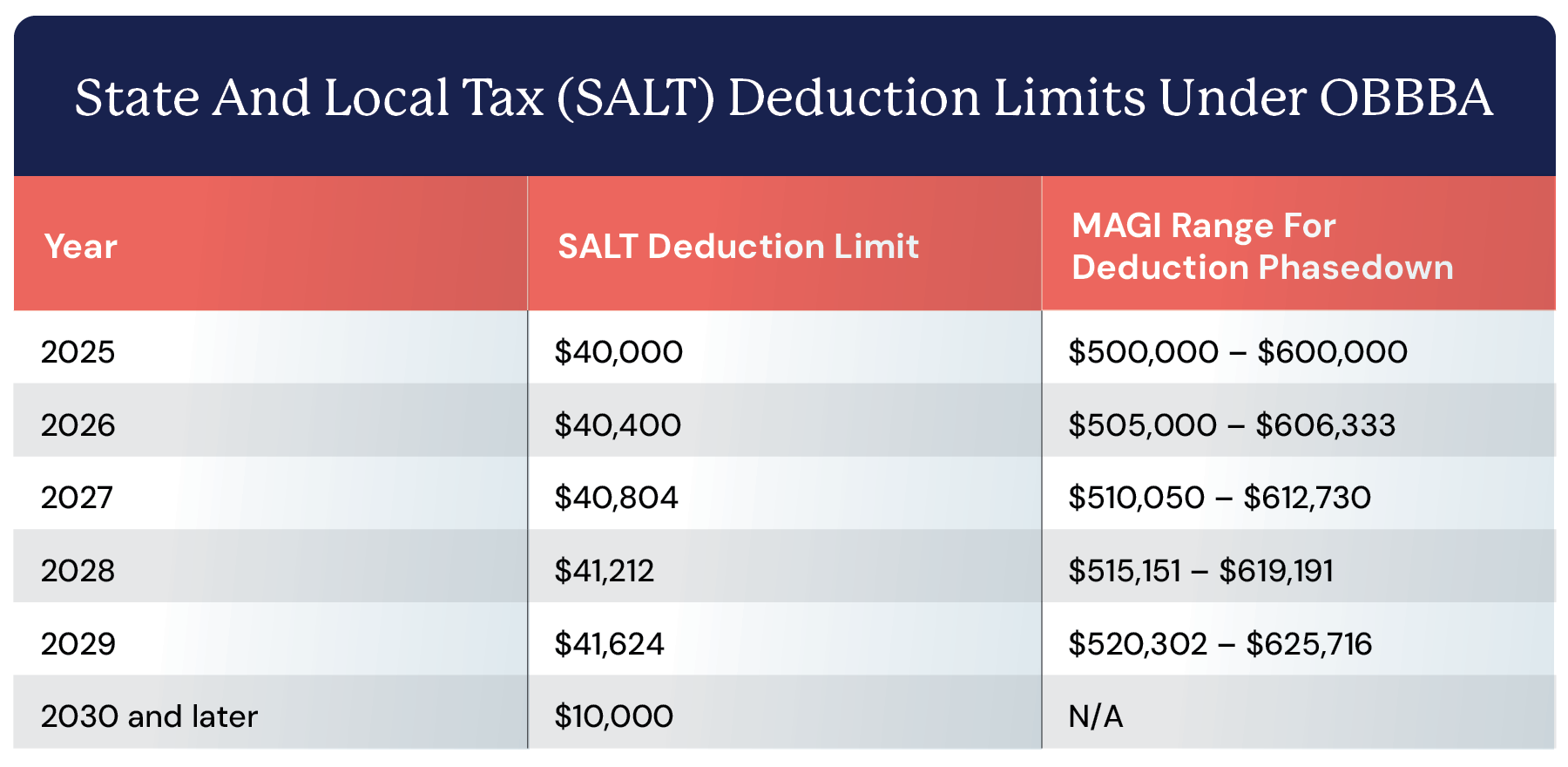

State and Local Tax (SALT) Deduction Temporarily Increased

High-income and property-focused households will appreciate OBBBA’s temporary expansion of the SALT deduction cap. From 2025 through 2029, the cap on the SALT deduction rises from the current $10,000 to $40,000 (indexed at 1% annually through 2029).

This deduction phases down for filers with MAGI above $500,000, and reducing to $10,000 when MAGI exceeds $600,000. Filers caught in that phasedown gap can face significantly higher effective marginal tax rates on any income recognized or deferred, but there are planning strategies that could be employed in this situation, such as bunching deductions into a single year.

The SALT deduction limit will drop back down to $10,000 for all filers in 2030 absent new legislation.

Tips & Overtime Deductions

The OBBBA doesn't actually eliminate taxes on tips, but rather creates a new below-the-line deduction of up to $25,000 for "qualified tip" income for single and joint filers from 2025-2028.

According to the law, the tips must come from an occupation that "traditionally and customarily" received tips prior to 2025; they must be voluntary and the amount determined solely by the payor; and they can't be earned through a Specified Service Trade or Business (SSTB), which has a specific definition under IRS code (and thus excludes some taxpayers that traditionally receive tips, such as musicians and entertainers).

Much like the tips provision, the OBBBA also creates a new deduction for qualified overtime income, effective from 2025-2028. Filers can deduct up to $12,500 (if filing single, head of household, or married filing separately) or $25,000 (joint filers) in overtime pay, defined as the amount of compensation paid above your normal rate. So, if you earned $30 in hourly base wages and $45 per hour for overtime, only the extra $15 an hour would qualify for the deduction.

Both the tips and overtime compensation deductions phase out starting at $150,000 MAGI for single filers and $300,000 for joint filers, and are available whether filers itemize or take the standard deduction.

Auto Loan Interest Deduction

Taxpayers may deduct up to $10,000 per year in qualified auto loan interest from 2025-2028, whether you itemize or take the standard deduction, but the provision only applies to new loans on new eligible vehicles—pre-owned vehicles do not qualify. The vehicle must also be assembled in the U.S., and purchased for personal use (not for business or resale).

The auto loan deduction begins phasing out for single filers with MAGI of $100,000, and joint filers with a MAGI of $200,000. The deduction completely phases out at $149,000 of MAGI and $249,000 of MAGI, respectively.

Other Notable Deduction Changes

The OBBBA retains the TCJA's cap on deductibility of mortgage interest paid on the first $750,000 of total mortgage indebtedness, but the OBBBA now allows mortgage insurance premiums to also be deducted.

If you’re in the top 37% federal income tax bracket, OBBBA also reduces the allowable amount of your itemized deductions. Beginning in 2026, allowable deductions will be trimmed so their tax benefit equals 35 cents on the dollar instead of 37 cents. The goal isn’t to take away deductions altogether, but to slightly narrow the benefit for the very highest earners. For example, under current law, a $100,000 of itemized deductions could save $37,000 in taxes. Under OBBBA, starting in 2026, the same amount of itemized deductions saves $35,000 in taxes.

OBBBA continues the Section 199A deduction of up to 20% for Qualified Business Income (QBI) with a few notable changes. Starting in 2026, the phaseout range is increased to $75,000 (single filers) and $150,000 (joint filers). Additionally, a new minimum deduction of $400 is created for individuals with at least $1000 of QBI.

Q. Do I need to worry about the Alternative Minimum Tax (AMT) again?

If you’re a high-income household, the short answer is yes—the Alternative Minimum Tax (AMT) is back on the radar under OBBBA.

Starting in 2026, the income threshold where the AMT exemption starts to phase out will drop to $500,000 for single filers and $1 million for joint filers (indexed annually). The exemption phaseout will also happen twice as fast at a rate of 50% of the dollar amount above the threshold, compared to the current 25% rate.

Why does this matter? With OBBBA increasing the standard deduction and temporarily raising the SALT deduction cap, some high-income earners—such as households with unexercised incentive stock options (ISOs)—could quickly find themselves nudged into AMT territory.

This also creates what we call “bump zones”: income ranges where each additional dollar doesn’t just get taxed at your normal marginal rate, but also reduces your AMT exemption. This can push your effective marginal tax rate above 40%, before you even add state taxes.

An important tool against AMT exposure is timing. If you expect a large income event, you may consider accelerating it into tax year 2025, before new thresholds and rules take effect. Or work with your adviser to spread taxable events over multiple years, if possible, to help avoid a “pile up” of taxable income in one year that potentially pushes you into a bump zone.

Q. Has the estate and gift tax exemption changed?

Yes. OBBBA continues the upward adjustment of the federal gift and estate tax exemption, which was first doubled to $11.2 million per person by the TCJA in 2018, and has since grown to $13.99 million per person in 2025. The new law increases that exemption to $15 million per person starting in 2026, with ongoing inflation indexing.

This is welcome news for families with sizable estates, as the exemption had been scheduled to be reduced by roughly half at the end of 2025 before OBBBA’s passing. If your family has already made significant gifts this year in anticipation of the lower exemption, it might be appropriate to revisit those plans—in some cases, by revisiting trust structures to better fit the new higher exemption. It’s best to review these strategies with a qualified tax or estate advisor to help plot possible paths here.

Some areas unchanged by OBBBA include the trust and estate tax brackets being locked in at 10%, 24%, 35%, and 37%, and the annual gift exclusion remaining at $19,000 for 2025, adjusted for inflation.

Q. Have there been changes to the buying or selling of property?

One change that will interest our rural and ag-minded clients relates to gains on qualified farmland sales. The OBBBA allows sellers to spread the gain from a sale of qualified farmland over four annual installments if it is sold to a "qualified farmer" (i.e., not a developer, but rather an individual who intends on farming the land). This can help ease the tax bite of a large sale concentrated in one year.

OBBBA also permanently restores 100% bonus depreciation for qualifying business property placed in service after January 19, 2025. That means businesses can immediately deduct the full cost of new machinery, equipment, or short-lived assets in the year they’re purchased. For ag producers and manufacturers, especially, this can be a significant cash flow benefit.

Q. How does charitable giving change under OBBBA?

For non-itemizers, there’s good news: Section 70424 of the OBBBA permanently restores the charitable deduction for taxpayers taking the standard deduction and doubles the pre-2020 limit. Beginning in 2026, you can deduct up to $1,000 (single filers) or up to $2,000 (joint filers) in qualifying cash contributions to charity each year—a straightforward way to capture some tax benefit from your giving.

For itemizers, starting in 2026, charitable contributions are only deductible to the extent they exceed 0.5% of your AGI. For example, a household with $1 million of AGI would see the first $5,000 of charitable gifts excluded from their federal deduction. You may carry forward the excess contributions beyond deductibility limits for up to five years. In addition, taxpayers in the top 37% bracket will see the value of all itemized deductions—including charitable contributions—capped at 35% of taxable income, further limiting the tax benefit of large gifts.

For donors at every level, these changes make timing and structuring your philanthropy more important than ever. Strategies such as bunching contributions into high-income years, using appreciated securities, or leveraging donor-advised funds can help preserve the tax efficiency of your charitable giving under the new rules.

Q. What are the new "Trump Accounts" for kids I've heard about?

The OBBBA creates a new type of IRA that can be opened and funded on behalf of any individual up until the year before they turn 18. These "Trump Accounts" offer an alternative to Traditional and Roth IRAs, which require earned income, and to 529 Plans, which are generally limited to qualified educational expenses (although some of that money could be rolled over into a Roth IRA).

Starting in 2026, families will be able to open Trump Accounts for their children; to jumpstart the program, the federal government will automatically contribute $1,000 for children born between 2025 and 2027. From there, families and employers can contribute up to $5,000 per year, with employers allowed to contribute as much as $2,500 toward an employee’s child’s account. Nonprofits can also make contributions, with no cap.

The funds may only be invested in qualified index funds and generally can’t be touched until the child turns 18, at which point the account is treated like a Traditional IRA and subject to standard IRA distribution rules. After age 59.5, the money can be accessed for any reason without early-withdrawal penalties. While contributions aren’t tax-deductible, the real advantage is the potential to grow tax-deferred from birth—giving kids the benefit of decades of compounded growth. Further guidance is still expected from the IRS for additional rules on Trump Accounts such as rollover, conversions, or Required Minimum Distributions (RMDs).

Want to learn more? Check out this story from KCRG-TV9 featuring our own Trent Von Ahsen and Bridget Davis talking about these new account types.

Planning Strategies with OBBBA

The complexities and scale of OBBBA make it difficult to understand all of its tax impacts across your financial plan. Some opportunities are obvious and immediate. For example, if you itemize and are planning a large charitable gift, 2025 is the year to do it before the new 0.5%-of-AGI floor takes effect in 2026. If you hold incentive stock options, exercising them before 2026 may help you avoid the tighter AMT thresholds ahead.

Other strategies will take time to crystalize. Some provisions start in 2025, like the new $40,000 SALT deduction cap and the $6,000 senior deduction, while others don’t begin until 2026, such as the itemized deduction limits for top earners and the adjusted phaseouts for the QBI deduction. With rules phasing in on different timelines, there may be additional strategies to implement in the coming years.

The bottom line: OBBBA is less about tax rates and more about timing. From 2025 through 2028, when the temporary deductions are in play, tax planning may be more complex than in years past. Specialized planning tools and careful coordination with income will be essential to avoid getting caught where phaseouts erase the benefit of deductions you thought you were receiving. This is where working closely with your adviser could add real value: translating new rules into strategies that keep more of your wealth working for you.

Ready to start your tax and financial planning journey with a team that actually understands tax implications? Reach out to us today and let’s have a conversation about how we can help set you up for success in the years ahead.

The commentary on this blog reflects the personal opinions, viewpoints, and analyses of Cedar Point Capital Partners (CPCP) employees providing such comments and should not be regarded as a description of advisory services provided by CPCP or performance returns of any CPCP client. The views reflected in the commentary are subject to change at any time without notice. Nothing on this blog constitutes investment advice, performance data or any recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Cedar Point Capital Partners manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results.